May 29, 2023 | Article

Everybody is “up in arms” about the new anti-money laundering and combatting of terrorist financing measures introduced which affect trusts. It is interesting to watch how many ‘so-called’ advisers see an opportunity to ‘make a quick buck’ by advising their clients to undo their trust structures, or out of complete ignorance themselves. The accounting and fiduciary industry has a responsibility to give (or obtain) the best advice for their clients and not, in a knee-jerk reaction to the new measures, blindly deregister trusts.

Although, in some instances, estate planners were ill-advised to register trusts in the ‘old days’, trusts were generally registered as part of estate plans. It takes a lot of effort to properly structure a trust and to effectively move assets into a trust as part of an estate plan. It will certainly trigger a number of costs and taxes (let alone the undoing of an estate plan) to give ill-considered advice. Estate planners should not lose sight of the purpose for which a trust was set up.

The benefit of having a trust as part of your estate plan will in most instances outweigh the extra layer of compliance costs as a result of the new measures. The following may serve as reminders of the reasons why estate planners may have been advised to register a trust. Do not undo your estate plan if it still makes sense to have a trust, but physically deregister the trust if it never served a purpose, as all trusts, whether dormant or not, fall under the same onerous measures, for which trustees may be fined and/or imprisoned.

Separate your personal assets from your business or property holding

The number one wealth preservation rule is to protect your assets. One of the most important reasons to consider a trust is because it will help you to separate your assets from your property investment debt, your business interests, and/or your other financial risks. Assets owned by a trust do not form part of the insolvent’s estate, and, therefore, cannot be attached by their creditors. However be mindful about how it is structured and how and when assets are moved into the trust.

Flexibility to cater for varying circumstances and events

A discretionary trust is extremely flexible and can be used to take into account any family, financial and legislative circumstances. This means that the trustees can manage the trust’s assets in the best interests of the beneficiaries, at any particular time, by taking into account all the relevant factors at that time. This flexibility caters for uncertainties such as divorce, insolvency, increase in family size or fortunes, and changes to tax legislation, provided the beneficiaries are defined, and the trust instrument is drafted in such a way as to anticipate these uncertainties. A trust also provides assistance for those tricky situations where people marry for a second or third time, and there are children from the previous marriage(s).

Family asset management

A trust can provide a centralised asset management structure, as well as controlled distributions for beneficiaries who are not in a position to manage assets themselves due to prodigality (excessive or extravagant spending). A trust can also provide for joint ownership of indivisible assets, such as holiday homes and farms. The benefit of ‘pooling’ a family’s wealth in a trust is that economies of scale can be reached, which may result in greater wealth growth over generations.

‘Insurance’ should something go wrong with your mental or physical health

In the event that a person may become mentally compromised, a trust should be considered to avoid placing that person under curatorship. A board of trustees, selected by the person, can then look after the financial affairs of that person instead of a curator, who may be a complete stranger appointed by the Court. From a tax perspective, the Income Tax Act makes provision for the creation of a Special Trust, where the trust is created for the benefit of a person who cannot take care of their personal affairs due to a disability, such as a serious mental illness. If you have created a trust during your lifetime and become afflicted by one of these dreadful conditions, your financial affairs would continue as before with persons that you entrust as trustees of the trust managing your affairs.

Preserve your wealth for future generations

If you bequeath your estate to individuals, it may become a case of easy come, easy go. For example, people who inherit, and/or their spouses, may not attach sentimental value towards the inheritance, and may put pressure on their spouses to liquidate the assets in order to go on an expensive holiday. Most people who have accumulated wealth in their lifetimes, or who have inherited wealth, prefer to see their wealth spread beyond the next generation. A trust is the most effective vehicle for the preservation of wealth. A well-run trust allows succeeding generations to participate in, and benefit from, the wealth created in one generation.

Protect other people

Often particular family members (such as people with disabilities) need special attention, and trusts are used to provide funds to look after those family members. Sometimes children have special challenges, which inhibit their ability to manage their own financial affairs. A trust is the perfect solution for such persons. This is also true for minors. Trusts for minors and disabled persons may enjoy special tax treatment.

Life continues for your family after death – no estate freezing

It is wise to arrange your affairs in such a way that when you are no longer here, your personal and financial affairs will continue with minimal disruption. Our heirs, who are usually traumatised by our departure, are then doubly traumatised by having to make decisions on matters that they have little or no knowledge of. An individual’s estate is frozen upon their death. It may take two or more years to finalise an estate, which could lead to financial hardship when the family cannot access any cash or assets until the estate has been wound up. This may be traumatic, especially when couples are married in community of property and their joint accounts are frozen, leaving the surviving spouse without access to any liquidity. In contrast, death does not interrupt the operation of a trust.

Protect your family from liquidity issues resulting from your death

Trusts provide liquidity solutions on death. On death, Estate Duty is payable on the value of the assets and Capital Gains Tax is payable on the growth of assets held in an individual’s hands, whether the asset is disposed of or held in the family. Executor’s Fees of 3.5% plus VAT of the gross asset value of the estate may also become payable. In a trust, Capital Gains Tax is only triggered on distribution or sale of the asset, hence matching tax liability to cash flow and not on anyone’s death. However, Estate Duty and Executor’s Fees will never be payable on assets in trust. For example, a family holiday home intended to be held for multiple generations would be better held in trust. Capital Gains Tax on the growth of the asset would only apply when the asset is actually sold by the trust.

~Source: Phia van der Spuy ~

Mar 3, 2023 | Article

Even though a trust is a unique entity, people often try to make sense of its nature by comparing it to a company, as a company is a well-known entity through which people operate their businesses.

Both a trustee and a director have similar fiduciary duties bestowed upon them. A fiduciary duty is an onerous, legal obligation (a duty of loyalty and care) of a person managing property or money belonging to another person to act in the best interests of such a person. These fiduciary duties are manifested either through the acts that govern trusts and companies, or by common law. Common law – also known as judicial precedent, judge-made law, or case law – is the body of law developed by judges and Courts. Common law stands on equal footing with statutes, which are adopted through the legislative process. The defining characteristic of common law is that it arises as a legal precedent that can be applied to similar situations.

A trustee, therefore, has to be more careful and cautious with the affairs of the trust than they would be with their own affairs. Whereas an individual can take personal risks in managing their own investments and affairs, they must take greater care when dealing with trust assets and avoid any business risk as far as possible (Sackville West v Nourse case of 1925). This view was confirmed in the Estate Richards v Nichol case of 1999, where it was stated that a person in a fiduciary position, such as a trustee, is obliged to adopt the standard of the prudent and careful person.

Fiduciary duties include the duty of care, diligence and skill, the duty to avoid conflict of interest (impartiality) and to act in the best interests of their shareholders and beneficiaries. The duties of trustees arise through the provisions of the Trust Property Control Act, our common law and the trust instrument.

It was held in the Doyle v Board of Executors case of 1999 that one of the principal characteristics of the office of trustee is that it is fiduciary in nature and that a trustee holds trust assets in a fiduciary capacity. The Court held that a trustee’s duty of “utmost good faith” towards all trust beneficiaries was pertinently founded on such trustee’s occupation of a fiduciary office and not from the trust instrument as held in the Hofer v Kevitt case of 1996. All trustees – whether independent or not – are charged with the responsibility of ensuring that the trust functions properly to the greatest benefit of the beneficiaries. The trustees owe a fiduciary duty to the beneficiaries of the trust – irrespective of whether the beneficiary has a vested right or is a contingent beneficiary whose right to trust income and capital will only vest on the happening of some uncertain future event (Griessel v de Kock case of 2019). A trustee’s fiduciary duty may require a trustee to obtain guidance from professionals when a particular matter does not fall within their skills or knowledge.

When considering the liabilities imposed on a director and trustee for breach of their duties, there is a clear difference between the liabilities imposed by the Companies Act and the Trust Property Control Act. Although the Companies Act comprehensively deals with liabilities should the director breach their duties, the Trust Property Control Act merely provides for the removal of a trustee and does not deal with further liabilities. The liabilities for breach of their fiduciary duties imposed onto trustees are based solely on our common law, because the Trust Property Control Act is not a complete codification of the law of trusts in South Africa.

An example of such a case is the van Zyl v Kaye case of 2014 that “Going behind the trust form, on the other hand, entails accepting that the trust exists, but disregarding for given purposes the ordinary consequences of its existence. This might entail holding the trustees personally liable for an obligation ostensibly undertaken in their capacity as trustees.”

The Master of the High Court regulates trusts by ensuring adherence to the wishes of the founder. If the trustees fail to do so, it may result in the removal of a trustee, request for security and/or appointment of a co-trustee. These measures require modification and updating to create stricter liabilities trustees should they fail in their duties. Currently there seems to be a lack of uniformity between court judgements.

A spouse, child, family member or family friend will often accept trusteeship without realising the burden that comes with it. Many people accept trusteeship but claim ignorance when things go wrong. All trustees are expected to actively participate in trust matters, and one is not allowed to leave the business of the trust in the hands of others. Be mindful, therefore, of using the services of a trust administrator, thinking that it excuses you from being actively involved in the management of the trust – because it does not!

Source: Phia van der Spuy

Mar 1, 2023 | Article

The JSE Slipped lower throughout Friday’s session, amid reports that South Africa has been greylisted by the Financial Action task Force (FATF).

Source: FNB Securities”

Dec 2, 2022 | Article

The timelines for winding up an estate have improved since the peak of the Covid-19 pandemic but are still likely to take longer than before Covid, as pandemic backlogs and other problems persist.

A year was a good expectation for an estate where the deceased left a sound will and the estate was dealt with by an experienced executor, Angelique Visser, Fiduciary Institute of Southern Africa (FISA) National Councillor, says.

During the pandemic, however, timelines deteriorated, making it common for any estate to take two years to wind up, FISA reported last year.

Increased deaths during the pandemic were responsible for much of the delays, but the offices of the Master of the High Court (the Master’s Offices) also took much longer to issue the letters that appoint executors, approve the estate accounts and authorise the distribution of estate assets to the heirs.

Bank delays frustrate estate professionals

Recently FISA has expressed its frustration with delays caused by banks and banks have admitted they too were slowed up by Covid and are still catching up.

To wind up an estate, the executor of the estate needs information about, among other things, your deceased family member’s bank accounts and investments.

The accounts then need to be closed and the balances or investments transferred into a bank account in the estate’s name.

The executor also needs the tax certificates for those accounts in order to file the deceased’s tax return and the estate’s return.

The chairperson of FISA, said banks are dragging their feet on these three tasks.

He says banks have different procedures which they sometimes change without consultation, leading to confusion among bank staff, as well as much frustration for FISA members trying to help families wind up estates.

Months to respond

Practitioners are now able to obtain a letter of executorship from the Master’s Office within two to three weeks, but then battle for three to four months for a response from some of the banks.

She says she has approached the senior management of several banks for assistance but there has been no improvement.

The chief executive officer of FNB Fiduciary, says COVID-19 negatively affected the industry’s processes for winding up deceased estates.

In addition to the increase in deaths, there has been an increase in fraud and administrative hurdles that are frequently beyond the control of executors and/or banks.

Banks are working through the Banking Association of South Africa with the Chief Master’s Office to address the challenges and minimise the adverse impact on the families of those who have died.

FNB is also trying to shorten the time it takes to wind up estates by increasing its capacity to help its clients and improving the processing of smaller estates using digital platforms, she says.

Two weeks to close account

Once the correct documents have been submitted, it should take 14 days to close an account and pay any money into the estate account.

Delays are primarily due to outages on the Master’s Office portal that banks and estate practitioners use and the need to get all the necessary documents from different parties. All of this has been compounded by the large volumes of estates currently experienced.

During the peak of the pandemic the Master’s Offices worked at 50% capacity and closed frequently when staff became ill. The offices and the Department of Justice’s computer system also suffered a ransomware attack in July 2021.

IT problems

The Master’s Offices are now open but continue to be plagued by computer problems, the recent FISA conference heard.

Martin Mafojane, the Chief Master of the High Court, said the Masters Offices do not have stable and reliable IT infrastructure resulting in the offices’ portal frequently being unavailable to professionals dealing with estates.

He said the offices fall within the Department of Justice and Constitutional Development which has now realised that rather than relying on contractors, it needs to recruit competent, qualified and skilful people to provide the tools that the offices require.

Confidence lost

Bongiwe Adonis, assistant manager at the Cape Town Master of the High Court, said the Master’s Office realised that practitioners and the public had lost confidence in it and that it needs to modernise its systems.

Online registration of deceased estates and trusts is one goal, and the aim is to have a user-friendly system like the South African Revenue Service’s eFiling system, enabling registration of an estate from anywhere in the world, she says.

But we are not there yet, an in the meantime, members of FISA, the Legal Practice Council and the South African Institute of Chartered Accountants can use a self-help system available at the Master’s Offices to register estates, she says.

The Master’s Offices have committed to processing applications registered this way within 10 days, Adonis says.

Estates that are not registered on this self-help system – for example when documents are couriered to the Masters Office have a 21-day turnaround time from the time, she said.

If the timeline is not met, the Master’s Office must explain the delay, she says.

Information is also being pulled from the Department of Home Affairs so that dependants can be identified and fraudulent activities minimised, Adonis says.

With these and other initiatives, the Master’s Offices are headed towards better and improved services by 2025, she says.

Source: FISA

Dec 2, 2022 | Article

Delport v Le Roux and Others [2022] ZAKZDHC 51

The applicant (D) brought an application under section 2(3) of the Wills Act, 7 of 1953 (the Act), asking the court to declare a document allegedly signed by the deceased (LR) as his last will and testament. The first respondent, the deceased’s estranged wife, had passed away by the time the case came to court. The second and third respondents (BR and BS) are the deceased’s daughters from a previous marriage, while the fourth respondent is the first respondent’s grandson who was adopted by the deceased and the first respondent. BR and BS opposed the application, while the fourth respondent did not. The fifth and sixth respondents, the Masters of The High Court in KwaZulu-Natal and Gauteng indicated that they will abide the decision of the court.

An accountant (SR) alleged in his affidavit that he drafted the document on instructions of the deceased and took it to the deceased, who signed it. SR then took the document to T, the wife of his business partner, and N to sign as witnesses. T and N were not in each other’s presence when they signed and neither of them was in the deceased’s presence when they signed as witnesses. It was therefore common cause that the document did not comply with the formality requirements for a valid will as provided for in section 2(1)(a) of the Act.

The lesson for fiduciary practitioners is to ensure that at all times that will documents are executed in strict accordance with the prescripts of section 2(1) of the Act.

In terms of s 2(1) of the Act the signature of the testator must be made in the presence of two or more competent witnesses. The witnesses must attest and sign the will in the presence of the testator and each other; where the testator signs the will with a mark, a commissioner of oaths must be present and specific certification formalities apply.

Nov 8, 2022 | Article

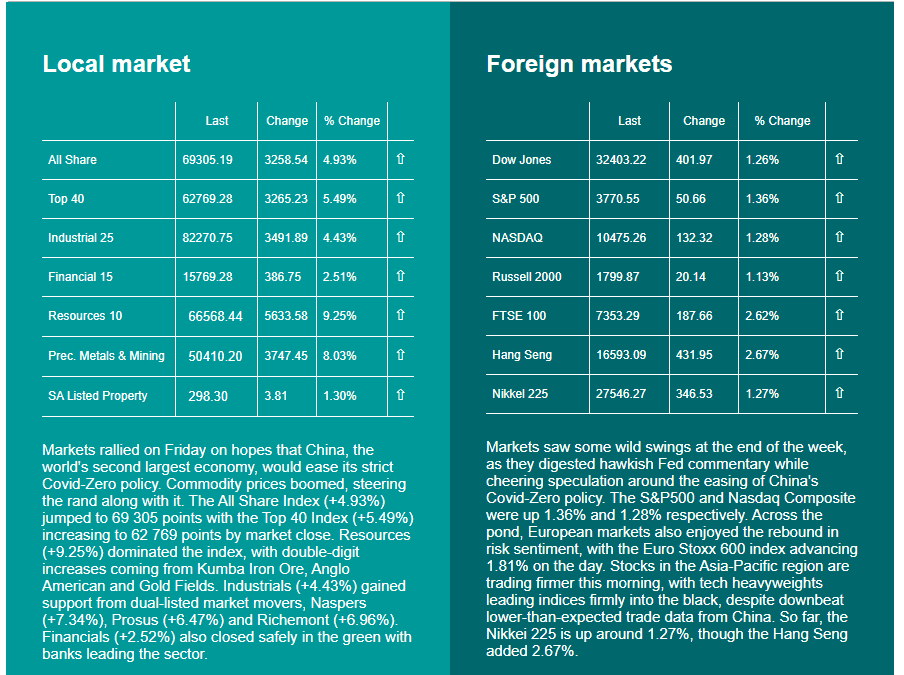

Markets rallied on Friday on hopes that China, the world’s second largest economy, would ease its strict Covid-Zero policy.

Recent Comments