Sep 19, 2022 | Article

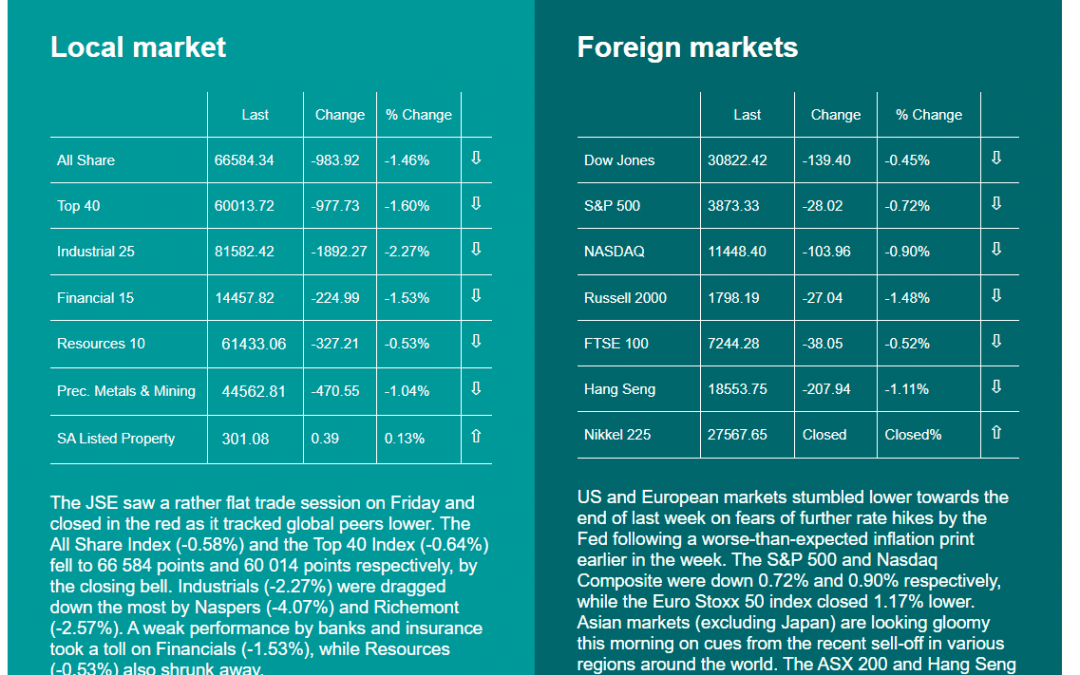

The JSE saw a rather flat trade session on Friday and closed in the red as it tracked global peers lower. The All Share Index (-0.58%) and the Top 40 Index (-0.64%) fell to 66 584 points and 60 014 points respectively, by the closing bell. Industrials (-2.27%) were dragged down the most by Naspers (-4.07%) and Richemont (-2.57%). A weak performance by banks and insurance took a toll on Financials (-1.53%), while Resources (-0.53%) also shrunk away.

US and European markets stumbled lower towards the end of last week on fears of further rate hikes by the Fed following a worse-than-expected inflation print earlier in the week. The S&P 500 and Nasdaq Composite were down 0.72% and 0.90% respectively, while the Euro Stoxx 50 index closed 1.17% lower. Asian markets (excluding Japan) are looking gloomy this morning on cues from the recent sell-off in various regions around the world. The ASX 200 and Hang Seng are trailing around 0.08% and 1.11% so far.

![Court case about trust assets and accrual upon divorce P A F v S C F [2022] ZASCA 101](https://agjenkins.co.za/wp-content/uploads/2022/09/AGJenkins-19.09.22a-1080x675.jpg)

Sep 19, 2022 | Article

The applicant (P) and the respondent (S) were married in 2001, out of community of property with inclusion of the accrual system. They were getting divorced in 2015. The divorce trial started on 18 February 2015.

Twenty days prior to the start of the trial P set up a trust in the British Virgin Islands (BVI) with their minor daughter as the only beneficiary and P’s brother, M, who was practising as a Queens Council in the BVI, as the only trustee. A day after the formation of the trust, P donated a sum of GBP115,000 to the trust. P’s version was that the trust was set up to cater for the minor daughter’s maintenance needs.

S averred that the setting up of the trust in the BVI was to make it more difficult for her to monitor the actions of the trustee or to take any action in case that was to become necessary. She also argued that the sum was placed in trust to frustrate her accrual claim. It was common cause that P’s estate experienced the greater accrual during the marriage.

The KwaZulu-Natal (Pietermaritzburg) High Court granted the divorce and ruled that the donation to the trust and the recording of an alleged loan by P’s father to him was done with the “fraudulent intention” to deprive S of her rightful accrual claim. The high court granted leave to appeal to a full bench of the KZN high court. The full bench dismissed the appeal.

P applied for special leave to appeal to the Supreme Court of Appeals (SCA). This application was done out of time and P had to apply for condonation of the late lodging of his application.

The SCA (Makgoka JA (Dambuza and Molemela JJA, and Makaula and Weiner AJJA concurring), held that there were no special circumstances why the late filing of the application should be condoned. The court also dealt with the prospects of success as part of the process and held that the timing of the setting up of the trust and the donation to the trust leads, in the absence of a reasonable explanation by P, to the conclusion that it was done to frustrate the accrual claim. The court also dealt with previous judgements about the nature of the court’s power to pierce the veneer of the trust and held that it is derived from common law and not from the Matrimonial Property Act or the Divorce Act.

As such the court held that the assets in the trust in the BVI should be taken into consideration in the calculation of the accrual claim. As there were no reasonable prospects of success, the late application for special leave to appeal to the SCA was dismissed with costs.

Sep 19, 2022 | Article

Some estate planners and trustees are not aware that a trust is regarded as a separate taxpayer, who has to register as such, and who has to submit relevant tax returns.

Trust income was always taxed in the hands of the trust unless it vested in the hands of the beneficiaries, whereby it was then taxed in the hands of the beneficiaries.

This practice was challenged in the CIR v Friedman case of 1993 on the grounds that the trust was not a taxable entity and, therefore, the trustees were not representative taxpayers. It was held in this case that, under common law, a trust is not a “person”.

This case resulted in the amendment to the definition of “person” in Section 1(1) of the Income Tax Act to include a trust and resulted in the inclusion of Section 25B in the Income Tax Act, which is a regulatory provision in the sense that it determines who will be taxed on trust income, and when, rather than being an anti-avoidance provision.

The principal taxing section for trusts

Section 25B of the Income Tax Act, which is the principal taxing section relating to trusts (subject to the anti-avoidance provisions of Section 7 of the Income Tax Act), provides that the income of a trust is taxed either in the trust or in the hands of the beneficiary as follows:

- If the income vests in a beneficiary during the financial year (ending February each year), then the beneficiary is taxed on it.

- If the income does not vest in the beneficiary, then the trust is taxed on it.

Section 25B of the Income Tax Act (referring to trust income) and Paragraph 80(2) of the Eighth Schedule to the Income Tax Act (referring to trust capital gains), read together with Section 7(1) (income distributed or vested but not yet paid) of the Income Tax Act essentially codified the Conduit Principle first articulated in South African common law.

That means that the Conduit Principle was first used without it being written into the Income Tax Act.

The Conduit Principle can only be used for taxing capital gains in the hands of the beneficiary if the trust instrument specifically gives the trustees the power to distribute a capital gain.

Wording to the following effect will empower the trustees to make a distribution of capital gains, which is an artificial concept in the Income Tax Act:

“…The trustees shall in their sole, absolute and unfettered discretion determine whether any distribution which represents the payment or distribution of any capital profit and/or capital gain arising out of the disposal of trust property, constitutes the vesting of an interest in the capital profit and/or capital gain in respect of that disposal for purposes of Paragraph 80(2) of the Eighth Schedule to the Income Tax Act 58 of 1962, as amended, irrespective of whether the amount actually distributed is lower or higher than the amount of the capital gain determined in respect of that disposal in terms of the Eighth Schedule to that Act.”

Do trusts pay provisional tax?

Trusts do not automatically qualify as provisional taxpayers in terms of Paragraph (1) of the Fourth Schedule to the Income Tax Act. They, therefore, must register with SARS as provisional taxpayers within twenty-one business days of becoming obliged to register – i.e. when they receive ‘income’ (note that this is a broader definition than ‘taxable income’).

Unless the trust distributes all income and/or capital gains in terms of the Conduit Principle discussed above, the trust will be liable to pay provisional taxes on amounts not distributed to beneficiaries or attributed to the funder.

All registered provisional taxpayers must submit a Provisional Tax Return (IRP6) and pay Provisional Tax twice a year in August and February each year. A top-up payment to pay 100% of the taxes due for that year may be made seven months after the year-end in August.

Provisional Tax is the only way that trusts would pay their taxes to SARS during the tax year if they earn taxable income. Although most trusts do not generate taxable income, SARS still requires nil income returns to be submitted.

If the trust does not qualify as a provisional taxpayer, but it derives a capital gain on the disposal of an asset during the year of assessment, then the receipt of the capital gain does not render it a provisional taxpayer.

When are trust tax returns due for submission?

Trust tax return due dates are in alignment with those of individuals. For this year the dates are as follows:

- Trusts that are not Provisional Taxpayers: 1 July 2022 to 24 October 2022; and

- Trusts that are Provisional Taxpayers: 1 July 2022 to 23 January 2023.

Source: Phia van der Spuy

Aug 26, 2022 | Article

Justice & Correctional Services Minister Ronald Lamola is confident the backlog in the Master’s Office – which accumulated during the Covid-19 pandemic and as a result of a September 2021 cyberattack – will be cleared by the end of December.

According to a Business Day report, Lamola told DA MP George Michalakis in June that there were 29 803 letters of executorship and letters of authority outstanding before 1 March 2022 and 9 102 trust registrations/appointments outstanding.

The Johannesburg office reported a backlog of 12 000 items of post. Replying to a question in the NCOP by Michalakis, Lamola said the office will work overtime to clear the backlog by the end of December. ‘It will, however, be noted that this target can only be achieved in an enabling and stable work environment,’ he said. ‘We are beginning to see improvement but not at the pace that is satisfactory, and we have registered that with the Chief Master. We have encouraged that employees should work overtime to address some of these challenges and backlogs.’ Making use of new technology would ensure expeditious processing and ensure that the backlog would not build up again, Lamola added. He insisted that the backlog had risen as a result of Covid-19 challenges and the hacking of the system, to which Michalakis replied: ‘We cannot forever blame Covid-19 and the hacking of the Master’s Office IT system.’

Recent Comments