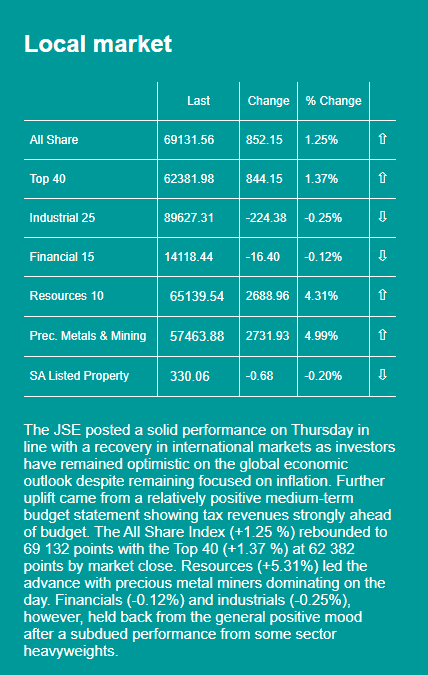

Our local markets have responded well to a relatively positive medium term budget statement

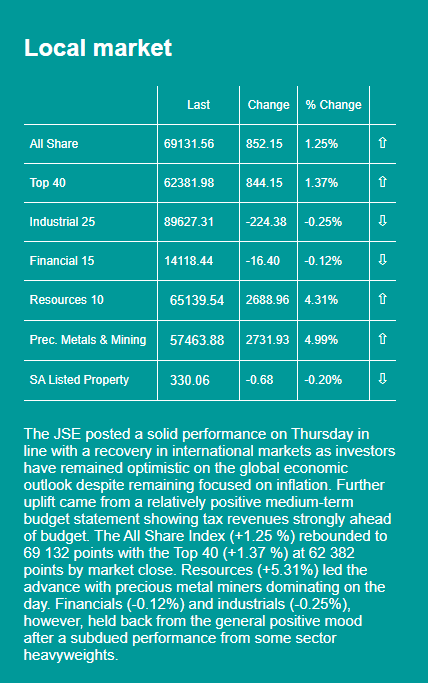

Our local markets have responded well to a relatively positive medium term budget statement

Source: FNB

Our local markets have responded well to a relatively positive medium term budget statement

Source: FNB

FISA issued the below press release today, 21 October 2021

Comment on the Master’s Office by the Fiduciary Institute of Southern Africa (FISA)

The public should be aware that there is an unprecedented backlog at the Master’s Offices countrywide. There are however some recent positive developments.

The Master of the High Court has been hard hit over the past 18 months by COVID closures and, more recently on 5 September 2021, a major cyber attack. These two developments combined have caused an almost total breakdown in services by the 15 Master’s Offices around the country.

There has been a recent positive development however in that the Master’s Office ICMS system has been restored, albeit on a sporadic basis, and has been accessed by some fiduciary practitioners.

It appears that Master’s Office officials are able to receive external messages, but it is currently uncertain whether all external messages are received. Furthermore, the offices can unfortunately not currently respond to queries, but might be in a position to respond telephonically, if the query is not reliant on the system.

Louis van Vuren, CEO of the Fiduciary Institute of Southern Africa (FISA) said that the public should be aware that processes which often take some time to be completed will be delayed yet further.

For example, the Master’s Office fulfils a crucial role in providing inter alia Letters of Executorship to executors of deceased estates, Letters of Authority to authorised trustees, and the approval of liquidation and distribution accounts in deceased estates. Banks use the Master’s Office portal to verify Letters of Executorship before they are willing to take instructions from executors regarding the bank account(s) of the deceased. This is a crucial step to enable the executor to make interim maintenance payments to a surviving spouse and/or children of the deceased. All these functions have essentially been on hold since 5 September.

Mr van Vuren said: “Trusts have also been badly affected. New or replacement trustees are not authorised which, if the trust deed requires a certain minimum number of trustees, means that the investment portfolios of trusts cannot be rebalanced and can be impacted negatively by market movements. In addition, testamentary trusts cannot be registered, leaving minor children without maintenance while new charitable trusts can also not be registered. The impact on society and the economy is therefore significant.”

He said: We would like the public to know that the problems are beyond FISA members’ remit, but we are willing to assist the Master’s Offices around the country as much as we can within the existing constraints.

https://www.fisa.net.za/press-release-fisa-comments-on-the-situation-at-the-masters-office/

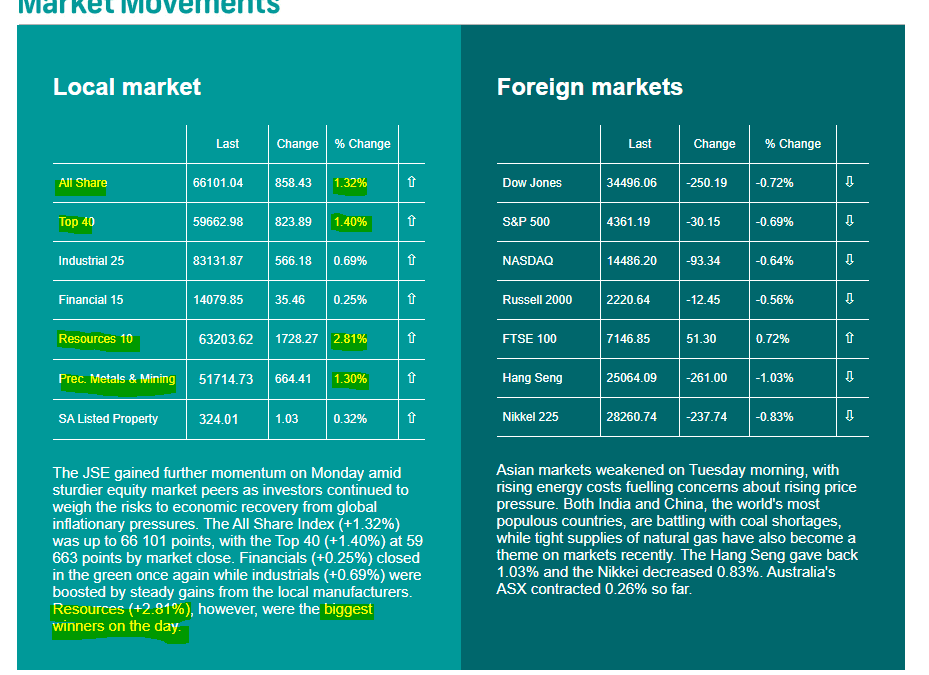

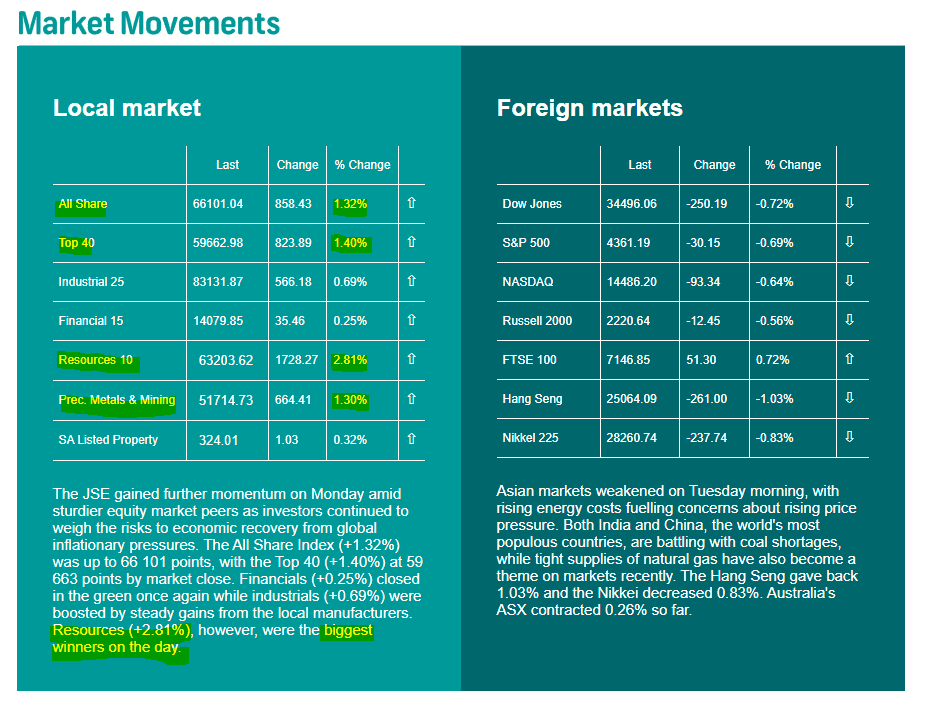

Yesterday saw pleasing positive movements in the local markets, particularly in Resourses and in Mineralsa and Mining.

In many instances, it may make sense to utilise existing trusts as part of your legacy plan.

Your assets can be bequeathed to an existing trust – if the trust instrument allows for it.

If this is the case, the trustees of that trust have to be specifically empowered in terms of the trust instrument to accept such a bequest.

Review the trustee power clause to ensure that the trustees can, in fact, accept further donations or bequests.

An obvious asset to bequeath to a trust is a loan owed by the trust to the testator or testatrix. Such loans typically originate from the sale of assets to a trust.

The testator or testatrix can also bequeath other assets to one or more existing trusts.

While it appears one can bequeath assets to both vesting and discretionary trusts (both ownership trusts, where the assets are held by the trustees for the benefit of beneficiaries), it is important to be mindful of certain principles.

Powers afforded to trustees

South African trust law distinguishes between a general and specific power of appointment afforded to a trustee.

The Braun v Blann & Botha case of 1984 established the principle that only a specific power of appointment of trustees is accepted or permitted.

If the trustees are granted powers that are too broad in terms of the trust instrument – such as the power to create further trusts as they wish or to include new beneficiaries (such as those not envisaged by the testator or testatrix when they drafted their will) – it may well be that the granting of such broad powers to trustees may pose a risk of attack on such trust by Sars, creditors and disgruntled beneficiaries.

Some even argue that a power to completely exclude a beneficiary from benefiting (as is the case with most discretionary trusts as it is the only way for it to qualify as a discretionary trust) from the trust may open a bequest to such trust to a risk of attack.

It is important to note that despite the fact that a bequest to a discretionary inter vivos trust (with broad trustee powers) may be open to attack, any attempt to empower trustees with an impermissible general power of appointment (unlimited discretionary powers) would, in any event, lead to the trust being declared invalid.

Bequest to existing vesting trust

A bequest to a vesting inter vivos trust was tested in the Kohlberg v Burnett case of 1986.

The testator bequeathed the residue of his estate to two trusts that he created about a year before his death.

It was claimed that the trust instrument did not form part of his will, that the bequest was a bequest to the beneficiaries under the trusts, that the identity of the beneficiaries could only be identified from the trust instrument, and that one cannot incorporate the terms of a document into one’s will by merely referring to it.

It was argued that the will failed to identify the beneficiaries of the bequest and that the assets would, therefore, devolve intestate.

The Court did not agree with this argument. It confirmed that a bequest to an inter vivos trust is valid without the terms of the trust being incorporated into the will, as required in terms of a testamentary trust.

It held that a trust is not a legal persona, but that trustees are entitled to act and hold property on behalf of a trust, that the beneficiaries of the bequests were the trusts which are clearly identifiable from the will, and that individuals who benefit in terms of the trust instrument are not beneficiaries in terms of the will, but rather in terms of the (existing) trust instrument.

It is important to note that the two existing trusts, in this case, vested certain rights in the beneficiaries.

The trust instruments gave clear instructions in terms of how the trustees were to deal with the income and capital of the trusts. In terms of the trust instruments, they had no discretion to deal with the income and capital of the trusts – it was, therefore, vesting trusts and not discretionary trusts.

In this case, there was no question of a delegation of testamentary powers – a principle that is not allowed in South African law.

Only a testator or testatrix can instruct how their assets should be dealt with post-death and no one else. The law does not allow a testator or testatrix to delegate their testamentary powers beyond certain limited exceptions – including through a trust structure.

What about existing discretionary trusts?

This case did not deal with discretionary trusts, where trustees have full discretion to deal with trust assets, which, in certain instances, may be equated to a delegation of testamentary powers.

It appears that it is the level of discretion afforded to the trustees in the trust instrument that is the determining factor in terms of whether a person can bequeath their assets to a discretionary inter vivos trust.

One would, therefore, need to study the terms of the trust instrument before bequeathing one’s assets to a discretionary trust and effect amendments if necessary.

For example, it is suggested that the beneficiaries (or even the trust instrument, which may affect the rights of beneficiaries or obligations of trustees) should not be allowed to be amended post the testator’s or testatrix’s death.

The trustees must be mindful and exercise extra care when dealing with assets bequeathed to a discretionary trust.

In summary, ensure the trust instrument allows for the receipt of bequests and that the trustees are not afforded too wide powers in the trust instrument, especially a right to amend beneficiaries or their rights.

By Phia van der Spuy

We are participating again in the National Wills Week

Contact us during the week of

13 – 17 September 2021

and we will draft or update your basic Will at no charge

It is highly advisable for the Founder/Donor/Settler of a new trust to ensure that there is a physical transfer of the asset/donation referred to in the trust deed as soon as the trust has been registered with the Master of the High Court and a bank account has been opened in the name of the trust.

Herewith a useful article by Phia van der Spuy dealing with this subject:

The trust assets defined in the trust instrument should be physically transferred by the founder to the trustees.

The founder has to relinquish control over the assets. The trust should be structured in such a way as to ensure there is a clear separation between control and ownership and enjoyment of trust assets. If that is not achieved, the trust may be at risk of attack.

In terms of the trust instrument, the founder is required to make an initial donation to the trust. In most cases, the founder stipulates an amount of money as the initial donation. Even if the amount is small (sometimes as little as R100), it must, by law, be deposited into the trust’s bank account. Under Section 11 of the Trust Property Control Act, the trustees are not allowed to hold the cash in their hands on behalf of the trust. Nor are they allowed to deposit the cash into a bank account that is not in the trust’s name.

The question arises whether it is a requirement for the founder to have transferred the initial donation to the trustees for the trust to come into existence.

Some people interpret the principle established in the Deedat versus The Master case of 1994 to mean that you do not have to make the initial physical donation to establish a trust, as long as there is an obligation to make such initial donation in the trust instrument, which is then made at a later date. The judge found in this case that “It may well be that the definition of a trust in the 1988 Act is wide enough to encompass property, duly identifiable, which is only to be acquired by the trustees in future from outside sources”.

The principle was confirmed in the Cunningham-Moorat versus Bester case of 2017, where the court ruled that it is not an essential factor for the formation of a valid trust that the trust assets (the initial donation) must be transferred to the trustees, but that a valid trust is legally recognised once it is registered with the Master of the High Court and the Letters of Authority issued. If the transfer does not happen, the trustees acquire the right to demand the initial donation from the founder – but the trust will exist.

It is, however, recommended to rather make the initial donation as soon as the trust is registered, in order to avoid attacks from the South African Revenue Service, creditors, and others.

Recent Comments