Dec 1, 2021 | Article

In the recent High Court judgment of Knuttel NO and Others v Shana and Others (GJ) (unreported case no 38683/2020, 27-8-2021) (Katzew AJ), the court had to decide whether the rules related to the commissioning of affidavits could be relaxed in certain circumstances.

The deponent to the founding affidavit was infected with COVID-19 at the time of deposing and certain extraordinary steps were taken for the commissioning of the oath. The question that essentially had to be answered was whether there was substantial compliance with the requirements for the commissioning of the oath to the founding affidavit and whether the extraordinary steps taken for the commissioning constituted substantial compliance with the requirements for the commissioning of oaths.

The respondents principally complained that the founding affidavit was not signed by the deponent in the presence of the Commissioner of Oaths (the commissioner) and that this conflicted with the Regulations Governing the Administering of an Oath or Affirmation (the Regulations), which were made by the Minister of Justice in terms of s 10(1)(b) of the Justices of the Peace and Commissioners of Oaths Act 16 of 1963 (the Act). The Act empowers the minister to make regulations prescribing the form and manner in which an oath or affirmation shall be administered, and a solemn or attested declaration shall be taken, when not prescribed by any other law. Regulation 3(1) requires that a deponent shall sign the declaration in the presence of the commissioner.

The legal practitioner on behalf of the applicant deposed to a separate affidavit wherein he gave a detailed explanation of the steps taken by him to ensure substantial compliance with the requirements in reg 3(1) and to ensure that the deponent to the founding affidavit signed in the presence of the commissioner, which, as already stated, was physically impossible due to the deponent’s infection with COVID-19 at the time.

The procedure followed by the legal practitioner can be summarised as follows:

- An unsigned draft founding affidavit was e-mailed to the deponent with instructions to read, initial and sign it before e-mailing it back to the legal practitioner.

- The legal practitioner then engaged the services of a commissioner who, in the legal practitioner’s presence in the office of the commissioner spoke to the deponent via a video WhatsApp call.

- Having identified the deponent as the person she professed to be, the commissioner then posed the usual questions before she administered the oath in the conventional way, except that the deponent initialled and signed the affidavit prior to the video call.

Considering the question posed, the court referred to the full court judgment of S v Munn 1973 (3) SA 734 (NC), which confirmed that the Regulations are directory only and that non-compliance would not invalidate an affidavit if there was substantial compliance with the formalities in such a way as to give effect to the purpose of obtaining the deponent’s signature to an affidavit. The Full Court in the Munn case found that the purpose of obtaining the deponent’s signature to an affidavit is primarily to obtain irrefutable evidence that the relevant deposition was indeed sworn to. Consequently, non-compliance with the Regulations does not per se invalidate an affidavit. As far back as 1973, the Munn case confirmed that the requirement of person-to-person physical presence between a commissioner and deponent is not peremptory and can be relaxed on proof on the facts of substantial compliance with the requirements.

In the case under discussion the court consequently held that there was substantial compliance with the requirement for person-to-person presence in administering the oath for the founding affidavit.

This finding is in line with foreign case law where judicial recognition has been given to the relaxation of the requirement of person-to-person presence for administering of an oath. In the case of Uramin (Incorporated in British Columbia) t/a Areva Resources Southern Africa v Perie 2017 (1) SA 236 (GJ), the court allowed the use of a video link to lead evidence in a civil matter from witnesses who were abroad. The judge administered the oath to them virtually before their evidence was led. Similarly, in the Canadian Superior Court of Justice (see Rabbat et al v Nadon et al 2020 ONSC 2933) the court permitted the virtual commissioning of affidavits considering the restrictions due to COVID-19.

The question of commissioning the oath without physical person-to-person presence arises more frequently in the digital era we live in. This judgment is a welcome guideline for litigants who require a departure from the rigidity of physical presence when commissioning affidavits. One would be well-advised to take heed of the judgment and the process followed therein should you be in a position, which requires some departure from the Regulations.

By Theo Steyn

Source: De Rebus

Nov 26, 2021 | Article

Gauteng High Court (Johannesburg) Judge Fiona Dippenaar has considered the better quality of life and opportunities in a foreign country in her decision to rule against a father who sought to scupper his five-year-old daughter’s imminent emigration with her mother. The Star reports Dippenaar presided over an urgent application brought by a mother identified as AK, father LKG and daughter A. The mother submitted before Dippenaar that she resorted to launching the urgent application because she had found a permanent job as a clinical psychologist in New Zealand. She contended that it was in A’s best interests to move to New Zealand because she had been the child’s primary caregiver since birth. LKG opposed the move on the grounds that it would severely prejudice his relationship with his daughter.

Dippenaar ruled that AK’s submissions had merit, notes the report in The Star. ‘In my view, it cannot be concluded that the relocation is not bona fide or reasonable. It can also not be concluded that the relocation decision was not taken bona fide,’ she said. ‘The opposition of the application on this basis lacks merit. The respondent has put up no primary facts which would justify the inferential conclusions he seeks to draw.’ Dippenaar pointed out that in addition to the fact that AK was a primary caregiver, it was a fact that she was relocating for greener pastures with her new nuclear family. ‘The applicant is a trained clinical psychologist who has secured a good position in the profession and the location of her choice,’ she said. ‘She is relocating with her nuclear family, a (new) husband, a (new) baby and A to pursue a new life in a secure location with free education and health-care programmes and a much lower unemployment rate than in SA.’

Dippenaar added: ‘Although it is in A’s best interests to have a good relationship with both her biological parents, the prejudice to her best interests if the relief sought is not granted, in my view, by far outweighs the prejudice if the relief is granted. It would be less detrimental to A not to deprive the applicant of the opportunity to relocate to New Zealand. It is open to the respondent to mitigate such prejudice to A by negotiating or obtaining generous access to A, albeit primarily virtually, at least on a day-to-day basis.’ Dippenaar terminated the parental rights that AK had to give or refuse consent to the child’s relocation

Source: LegalBrief

Nov 26, 2021 | Article

This is a useful article by Phia van der Spuy dealing with this topic:

Trustees should act in the best interests of all the beneficiaries, in line with the terms of the trust instrument. In the Griessel v de Kock case of 2019 the Court held that the “role of a trustee in administering a trust calls for the exercise of a fiduciary duty owed to all the beneficiaries of a trust, irrespective of whether they have vested rights or are contingent beneficiaries whose rights to the trust income or capital will only vest on the happening of some uncertain future event”. If income and capital beneficiaries are not the same people, it may present a potential conflict which the trustees would have to manage.

Define beneficiaries well

Beneficiaries are the only persons who can ever benefit from a trust. There is flexibility regarding how the estate planner can arrange who is to benefit from the trust assets. For a start, one can distinguish between those who can benefit from the capital (the assets) of the trust and those who can benefit from the income generated by assets in the trust. One can also ‘vest’ income and/or capital in one or more beneficiaries (which they are entitled to), or only give one or more beneficiaries discretionary or contingent rights (only a hope to receive something) to trust income and/or capital until the trustees have exercised their discretion in favour of such beneficiaries, upon which such distribution vests in the beneficiaries. In some trusts, beneficiaries may have a combination of rights, such as vested rights to trust income and discretionary rights to trust capital (which beneficiaries hope to receive), or vice versa. This mechanism provides the estate planner with an opportunity to specify which beneficiaries should receive which benefits (income and/or capital) from the trust. This is a personal preference and choice of the estate planner, which needs to be carefully considered by them when the trust is registered.

Potential conflict between different types of beneficiaries

When capital and income beneficiaries are different people, extra care should be taken to ensure that all beneficiaries’ needs are considered. Capital beneficiaries may prefer capital growth and capital preservation, while income beneficiaries may favour maximising income, even if it is at the cost of capital growth or capital preservation. The apportionment of expenses to income and capital beneficiaries may also become a challenge when attempting to establish fairness.

Possible solution

Income should be clearly distinguished from capital in the trust instrument, especially if different people are income and capital beneficiaries. Be mindful how you define ‘income’ in the trust instrument since it may include all ‘fruits’ from assets – such as the occupation of a property – or it can narrowly refer to actual revenue received, such as rental income. The term ‘net income’ – gross income less expenses – should also be clearly defined, and the trust instrument should allow trustees to distribute both income and net income to capitalise on the benefit of the ‘conduit principle’. If only income is distributed, the expenses related to the income will not be capable of deduction for tax purposes in the hands of the beneficiary or the trust and will be lost. Capital beneficiaries, on the other hand, may benefit from the distribution of an actual trust asset or from a gain made on the disposal of trust assets, depending on its definition in the trust instrument.

The treatment of unallocated income should also be defined to reflect the founder’s intention – in other words, whether it will form part of trust capital at the end of a financial year, if unallocated, or whether it will keep its nature as income. If the trust instrument is silent, it may be assumed that income and capital will always retain their individual natures.

In the event that income and capital beneficiaries are different, it is good practice to state in the trust instrument that if the income is insufficient for the maintenance of an income beneficiary that trust capital can be used to make good on any such shortfall. This will assist the trustees in optimising the trust’s investment returns while taking into account the needs of all beneficiaries to prevent unintended hardship. Focusing solely on a trust’s short-term income production may have a detrimental effect on the long-term position and value of the trust’s assets, which, in the long run, may negatively impact both the income and capital beneficiaries.

Advice to trustees

Part of the process of taking control of the trust assets is to ensure that money in the trust is properly invested. The trustees begin this process by establishing, where possible, the intention of the founder of the trust. They would then establish the needs of each of the beneficiaries. The trustees are required to establish the short, medium and long-term requirements of the income beneficiaries, as well as those of the capital beneficiaries. Once the needs of the beneficiaries have been established, negotiated, and agreed upon, the trustees can then ascertain their investment powers before making an appropriate investment.

In the Sackville West v Nourse case of 1925, the beneficiary succeeded in a claim for damages for negligence against a trustee who had made an unwise investment. The trustees, therefore, have to perform a delicate balancing act between seeking out safe investments and avoiding risk, versus investing trust assets productively while considering beneficiary needs – for both income and capital beneficiaries. Since an element of risk-taking seems unavoidable, trustees should record and document their reasons in arriving at investment decisions.

~ Written by Phia van der Spuy ~

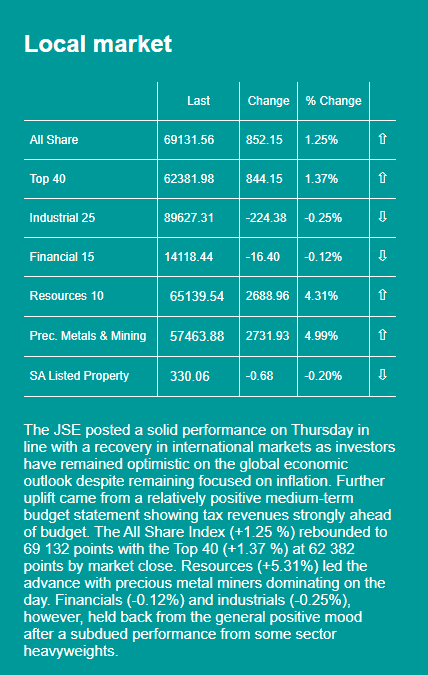

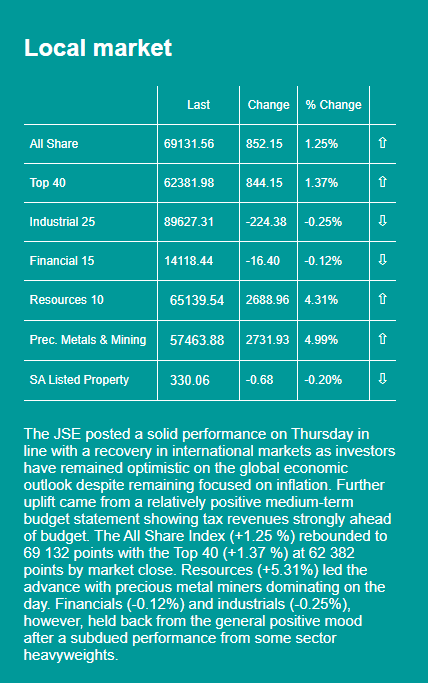

Nov 12, 2021 | Article

Our local markets have responded well to a relatively positive medium term budget statement

Source: FNB

Oct 22, 2021 | Article

FISA issued the below press release today, 21 October 2021

Comment on the Master’s Office by the Fiduciary Institute of Southern Africa (FISA)

The public should be aware that there is an unprecedented backlog at the Master’s Offices countrywide. There are however some recent positive developments.

The Master of the High Court has been hard hit over the past 18 months by COVID closures and, more recently on 5 September 2021, a major cyber attack. These two developments combined have caused an almost total breakdown in services by the 15 Master’s Offices around the country.

There has been a recent positive development however in that the Master’s Office ICMS system has been restored, albeit on a sporadic basis, and has been accessed by some fiduciary practitioners.

It appears that Master’s Office officials are able to receive external messages, but it is currently uncertain whether all external messages are received. Furthermore, the offices can unfortunately not currently respond to queries, but might be in a position to respond telephonically, if the query is not reliant on the system.

Louis van Vuren, CEO of the Fiduciary Institute of Southern Africa (FISA) said that the public should be aware that processes which often take some time to be completed will be delayed yet further.

For example, the Master’s Office fulfils a crucial role in providing inter alia Letters of Executorship to executors of deceased estates, Letters of Authority to authorised trustees, and the approval of liquidation and distribution accounts in deceased estates. Banks use the Master’s Office portal to verify Letters of Executorship before they are willing to take instructions from executors regarding the bank account(s) of the deceased. This is a crucial step to enable the executor to make interim maintenance payments to a surviving spouse and/or children of the deceased. All these functions have essentially been on hold since 5 September.

Mr van Vuren said: “Trusts have also been badly affected. New or replacement trustees are not authorised which, if the trust deed requires a certain minimum number of trustees, means that the investment portfolios of trusts cannot be rebalanced and can be impacted negatively by market movements. In addition, testamentary trusts cannot be registered, leaving minor children without maintenance while new charitable trusts can also not be registered. The impact on society and the economy is therefore significant.”

He said: We would like the public to know that the problems are beyond FISA members’ remit, but we are willing to assist the Master’s Offices around the country as much as we can within the existing constraints.

https://www.fisa.net.za/press-release-fisa-comments-on-the-situation-at-the-masters-office/

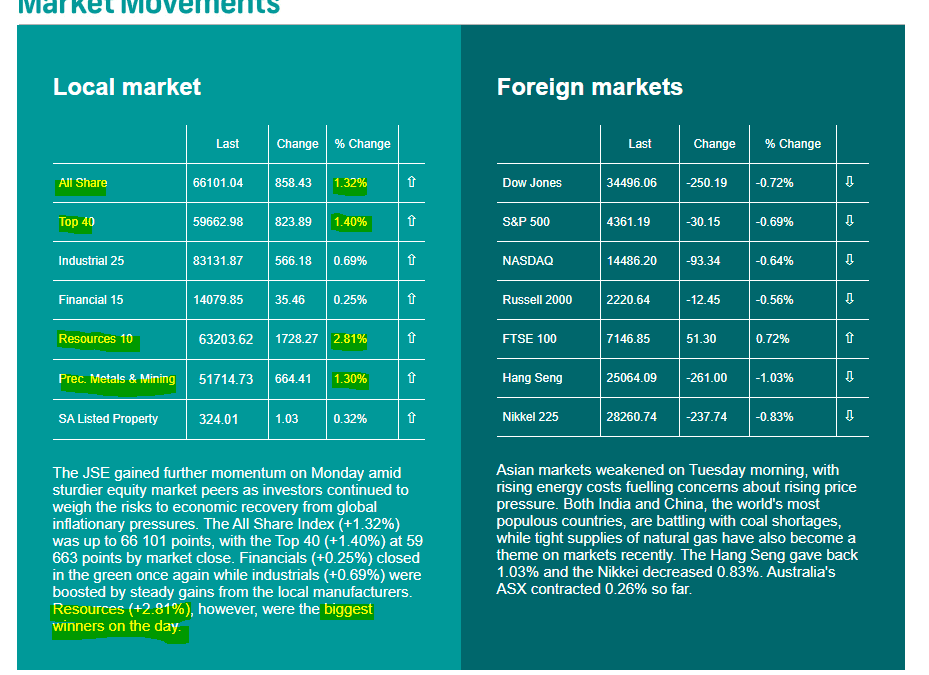

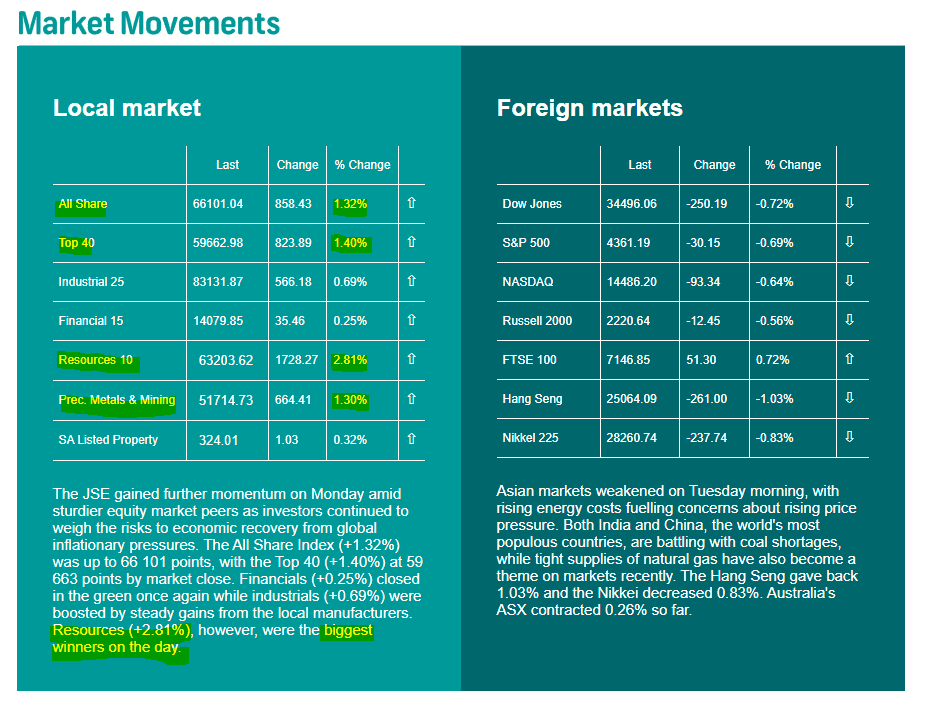

Oct 12, 2021 | Article

Yesterday saw pleasing positive movements in the local markets, particularly in Resourses and in Mineralsa and Mining.

Recent Comments