Aug 20, 2021 | Article

ALL ABOUT TRUSTS:

It often happens that trustees do not actively participate in trust matters on an on-going basis – such as when soon-to-be-ex-spouses do not want to face one another in trustee meetings, or when people simply rely on an (invalid) clause in a trust instrument to abdicate their responsibility as trustee. Here’s a closer look at what our law allows.

Alternate trustee

A trust instrument may allow the use of an alternate trustee in the event that an appointed trustee cannot attend a meeting or is temporarily absent and cannot participate in the trust’s affairs. Even if the trust instrument allows for the use of a temporary alternate trustee, the actions by the alternate trustee may be null and void for the following reasons:

- Section 6 of the Trust Property Control Act requires a person to be duly authorised by the Master of the High Court before they can act as a trustee of the trust. The Act does not make provision for the appointment of an alternate trustee.

- Our common law requires all trust decisions to be made by duly appointed trustees of the trust, and no one else.

- There is no room in our law for a “silent” or “sleeping” trustee who appoints someone else to act on his or her behalf.

A trustee cannot empower an alternate trustee to act on his or her behalf to exercise a general discretion and decision-making which vests in the trustee. Alternate trustees can, therefore, not make decisions as they wish. A stipulation in the trust instrument allowing a proxy (see below) or alternate trustee to vote as they “may deem fit”, results in an abdication of a trustee’s powers, which is not allowed. If an alternate trustee is allowed to exercise their independent judgement and form a personal view at a trustees meeting, he or she would be allowed to act like an appointed trustee, without being duly authorised, as required under Section 6 of the Act (Hoosen v Deedat case of 1999).

A proxy

A possible solution for a trustee who cannot attend a meeting is the use of a proxy. A proxy is a written authorisation from an absent trustee that grants a limited power of attorney to another person (the proxy) to vote on behalf of and in accordance with the directions of the trustee.

A proxy allows a duly authorised person to represent a trustee at a meeting if it is specifically allowed in the trust instrument. The court held in the Malatji v Ledwaba case of 2021 that there is no common-law principle allowing representation by proxy. If the trust instrument does not specifically allow for the use of a proxy, the parties have to be present in person at the meeting to be entitled to vote. The court held further that a proxy is a form of a mandate, and requires a mandate to be extended by the principal to an agent to exercise the vote to which the principal was entitled at the meeting. The votes “by proxy” on behalf of the deceased and absent beneficiaries were therefore not allowed in terms of our common law and in conflict with the provisions of the trust instrument.

Such a proxy can merely act as the messenger of the trustee they represent and convey the thoughts and/or votes of the trustee who granted the proxy. A stipulation in the trust instrument allowing a proxy to vote as they “may deem fit”, results in an abdication of a trustee’s powers, which is not allowed. If a proxy is allowed to exercise his or her independent judgement and forms a personal view at a trustees meeting, the proxy would be acting a trustee of the trust, without being duly appointed as trustee, as required in terms of the Act.

Even if another trustee of the trust acts as a proxy for a trustee, allowing such a person to act and decide as they wish is not allowed, as it would result in an abdication of power to the proxy.

Although the Steyn v Blockpave case of 2011 accepts that a trustee who cannot personally attend a meeting can make use of a proxy, it must not be broadly interpreted. Only the use of a proxy as described above will result in valid decisions taken by the board of trustees.

No delegation of authority

Trustees may delegate tasks (in other words, they may execute decisions already taken by the board of trustees), but they are still required to make decisions and exercise discretionary powers personally and independently, without the influence of any other person. In the Hoosen v Deedat case, the court held that a trustee who is chosen because of a certain special quality or ability may not delegate their powers, authority, or duties to anyone else. The court emphasised that a trustee cannot abdicate his or her powers and, in so doing, be released from the responsibility as a trustee. No act of a person, while acting as a trustee, will indemnify them against the liability for breach of trust where they fail to show the degree of care, diligence and skill required in terms of Section 9(1) of the Act.

It is clear that the fact that trust instruments, in many cases, contain a general stipulation that the trustees shall have unlimited or unfettered discretion, does not allow them to do as they please. They have to be able to prove that they remain involved in all trust matters, that they have applied their minds, and that they always act in the best interests of the beneficiaries.

Phia van der Spuy

Jul 21, 2021 | Article

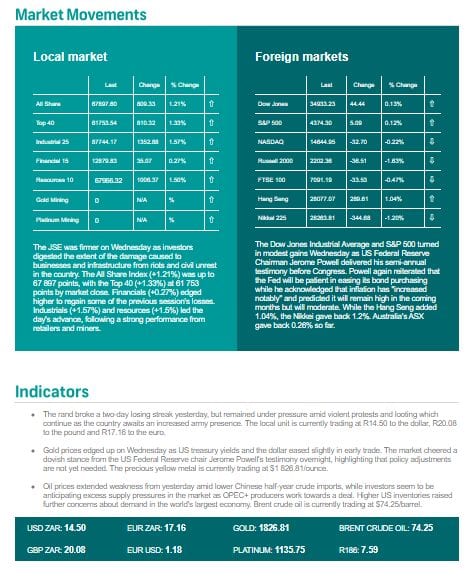

We saw a slight uptick on the local markets yesterday, after a volatile week.

Jul 18, 2021 | Article

As is sadly all too frequent, wills can trigger family disputes on the death of the testator.

An extreme example of this is the Miramar murders which took place in Tapei in 2016; an alleged double murder and suicide resulted in the death of three brothers, all members of a prominent Taipei family. The late Tycoon Huang Jung-tu, the brother’s father, had amassed a colossal business empire estimated to be worth US$3 billion, which included the famous hotel and retail chain empire, known as the Miramar Group. The shootings occurred in November 2016 at a corporate meeting in the headquarters of part of this empire, the Mayfull Food Corp, one of Taiwan’s major meat importers and distributors. At the meeting, chaos ensued following the discussion about how to split the inheritance of the business left by their father; the younger brother reportedly took out a pistol and shot two of his brothers before he committed suicide with a single shot to his head.

A further complication was the family dynamic; the late father had been married twice with seven sons, and had a further two sons from another relationship, creating a myriad of obstacles!

How to avoid disputes in inheritance

Talks about inheritance need not end in murder! Many do, however, end in disputes because no will or succession plan has been put in place. The current pandemic has encouraged more people to address their wills. There are still, unfortunately, an overwhelming majority of individuals whose wills are not up-to-date and therefore do not reflect their current intentions.

For individuals with assets placed in other countries it is even more crucial to have a will, or to have more than one will.

Should individuals invest in one or more wills?

Depending on the circumstance, it can be appropriate to have one will covering worldwide assets. In others, it is advisable to have more than one will – an “international” or “offshore” will or wills.

A substantial benefit of having an offshore will is that, rather than being required to wait for a will to be submitted in the home jurisdiction before the offshore assets can be administered, the offshore will can be submitted simultaneously to that of the home will. The estate should be finalised quicker, and at a reduced cost. In Jersey, for example, the person entitled to administer the estate is required to make a personal appearance at the jurisdiction’s Court to swear the oath. If they are unable or unwilling to fly to Jersey, a local agent will need to be appointed in order to attend the Court on their behalf. It is, on the other hand, a far more time- and cost-effective way of handling a Jersey estate if there is a Jersey will that appoints a local executor, for example a Jersey lawyer.

Furthermore, some jurisdictions have marital regimes which impact inheritance. This is the case in Italy and can mean, firstly, that assets in the sole name of one spouse are, effectively, owned jointly by both spouses and, additionally, that those assets might not be free to dispose of by will.

It can also be the case that an offshore will has been drafted in accordance with offshore estate planning advice. The will can therefore utilise any available tax planning opportunities, or reduce or avoid offshore probate fees.

Another benefit is that where the offshore asset is a property, an offshore will can minimise difficulties in relation to the succession to the property. From a practical standpoint, the offshore will can be drafted in the local language, use local terminology and nuances, and so avoid any potential problems of drafting a will which does not work. English wills, for example, often include trusts which are, usually, not recognised in civil law jurisdictions such as France and Spain. Furthermore, some jurisdictions have forced heirship rules; this means that assets in that jurisdiction can only pass in a prescribed manner. On some occasions an offshore will can override such rules, but the home will can compensate for this by seeking to balance out the distribution of the estate overall.

Other advantages are demonstrated by South African wills; these include a clause specifying how much can be charged to administer the estate, as a percentage. This is a binding agreement and can be negotiated to reduce the cost. There can be exchange control concerns where, typically, the individual does not want offshore assets going to South Africa as part of the administration of the estate because there are restrictions on how much can be taken out of South Africa. It should be noted that the South African exchange control rules are changing, and it is best to always seek local advice.

Risks associated with offshore wills

While there are certain disadvantages associated with offshore wills, such as the risks of accidental revocation and partial intestacy, these can be reduced by careful drafting and good advice. Likewise, although it may cost more money to have more than one will initially, the additional costs are offset by the money that the estate saves as the result of having a more streamlined estate administration.

Jonathan Colclough, Fisa member and Partner, BDB Pitmans, UK.

Jul 15, 2021 | Article

Jul 12, 2021 | Article

This is a very useful article by Phia van der Spuy and it is important to bear in mind the Transfer Duty implications for the acquirer of immovable property from the Trustees in certain circumstance.

TRANSFER Duty is an indirect tax levied on the acquisition of fixed property in South Africa.

It is payable on the value of any property acquired by a person by way of a transaction or in any other manner. Transfer Duty is not payable on the transfer of the property that gave rise to Transfer Duty.

Instead, it is the acquisition of the personal right by the purchaser against the seller that gives rise to the Transfer Duty obligation. The Court held in the CIR versus Freddies Consolidated Mines Ltd case of 1957 that the word “acquired” (which is required for a “transaction” to take place under the Transfer Duty Act) means the acquisition of a “right to acquire ownership in a property”.

The judge confirmed in the SIR versus Hartzenberg case of 1966 that Transfer Duty becomes payable upon the acquisition by a person of a personal right to obtain dominium (ownership and control) in immovable property.

With a vesting trust where the beneficiary has a vested right in the trust income (both of a revenue and capital nature) and/or capital in terms of the trust instrument, or a discretionary trust where the trustees exercised their discretion in favour of the beneficiary and the beneficiary obtained a vested right in the trust capital, they will obtain only a personal right against the trustees.

No Transfer Duty is payable when a beneficiary obtains a personal right from the vesting of trust capital because no specific property was vested. Even though a beneficiary may have a vested right in trust capital, the trustees may (if they are entitled to do so under the provisions of the trust instrument) decide to sell the property (and even buy another in its place). In this case, it is clear that the beneficiary never had a real right in either of the properties while they were registered in the names of the trustees.

Only when the trustees decide to transfer a property to a beneficiary do they acquire a real right. This might never happen if the trustees decide to sell and convert the property into cash and then distribute such cash to the beneficiaries. The beneficiary will obtain a real right in the trust asset as soon as ownership in such asset is transferred to the beneficiary. If property is transferred to the beneficiary, they will be liable for Transfer Duty once it is transferred.

In the event of the trustees electing to vest immovable property in the name of a beneficiary of an ownership inter vivos trust (which includes a vesting trust and a discretionary trust) by transferring the property into the name of that beneficiary in the Deeds Registry, the transfer is exempt from Transfer Duty provided the beneficiary is related to the founder or creator of the trust by blood within three degrees of consanguinity and the beneficiary paid no consideration (directly or indirectly) for the property (Section 9(4)(b) of the Transfer Duty Act).

In the event of the trustees electing to vest immovable property in the name of a beneficiary of a testamentary trust by transferring the property into the name of that beneficiary in the Deeds Registry, the transfer is exempt from Transfer Duty provided the beneficiary is entitled to it under the will in terms of which the trust was set up. (Section 9(4)(b) of the Transfer Duty Act).

Beneficiaries are not the owners of the trust assets in an ownership trust (which includes a vesting trust and a discretionary trust), but have a vested right with regard to any capital distributed by the trustees.

If a beneficiary disposes of this right, it is not a “real right in land” or a “contingent right in a discretionary trust” and, therefore, does not fall within the ambit of “property” as defined in Section 1 of the Transfer Duty Act.

However, when a beneficiary disposes of their contingent right in a discretionary trust – such as when beneficiaries are substituted during the amendment of a trust instrument – not only may it be argued that a new trust may have come into existence as a result thereof (with Capital Gains Tax and other potential tax consequences), but it may trigger Transfer Duty as a result of the “substitution or addition of one or more beneficiaries with a contingent right to any property of that trust, which constitutes residential property”(Section 1 of the Transfer Duty Act).

Since there is no definition of “residential property trust”, the provisions would apply to a trust owning residential property regardless of the proportion of such property to the full value of the assets held by the trust. In this instance, the Transfer Duty is based on the full market value of the residential property, regardless of the interest the person acquires in the trust.

Therefore, any indirect transfer of immovable residential property (primarily to avoid Transfer Duty) becomes taxable in the same manner as any direct transfer of the property out of the trust.

![Court case: Handwritten document not intended to be a will – Osman and Others v Nana N.O and Another [2021]](https://agjenkins.co.za/wp-content/uploads/2021/07/agjenkins-Article-court-case-1080x675.jpg)

Jul 12, 2021 | Article

Osman and Others v Nana N.O and Another [2021] ZAGPJHC 47

The deceased (S) died in April 2018, apparently without a valid will. He was a medical doctor. The first respondent (N), one of the daughters of S, was appointed as executor of the deceased estate by the Master of the High Court at the end of June 2018. Under intestate succession N and her siblings would be the only heirs of the residue of the deceased estate. The eighth appellant, Y, is the son of one of S’s sisters. On 1 August 2018 Y searched the former home of S and found a document entitled “Notes on will” dated 14 August 1990. The document was handwritten and unsigned.

The sisters of S brought an application to have the handwritten and unsigned document declared a valid will under the provisions of section 2(3) of the Wills Act, 7 of 1953. The section reads:

“If a court is satisfied that a document or the amendment of a document drafted or executed by a person who has died since the drafting or execution thereof, was intended to be his will or an amendment of his will, the court shall order the Master to accept that document, or that document as amended, for the purposes of the Administration of Estates Act, 1965 (Act No. 66 of 1965), as a will, although it does not comply with all the formalities for the execution or amendment of wills referred to in subsection (1).”

The court a quo (Matojane J) dismissed the application and ordered costs to be paid from the deceased estate. The court held that although it was not in dispute that S wrote the document in his own hand and therefore drafted the document, there is no evidence that he intended the document to be his will. Therefore the second requirement of section 2(3) was not fulfilled.

On appeal to a full bench of the Gauteng High Court, the court (Meyer J (Windell and Twala JJ concurring) dismissed the appeal with costs. The court was critical of the lack of evidence and failure to supply facts supporting the notion that S intended the document to be his will and the fact that the appeal was aimed against the whole of the court a quo’s judgement and order.

Recent Comments